Introduction to Credit Guarantees

Over the years, risk-sharing mechanisms such as insurance, guarantee schemes, contractual agreements, and financial derivatives have distributed potential losses among parties, reducing the burden on any single participant. Globally, credit guarantee schemes have grown significantly, addressing credit gaps for Small and Medium Enterprises (SMEs) and development projects. Credit guarantees enhance debt instruments like loans or bonds by de-risking them. They represent binding promises from guarantors to pay a pre-determined amount (up to 100% coverage) for principal and/or interest upon default by the primary obligor.

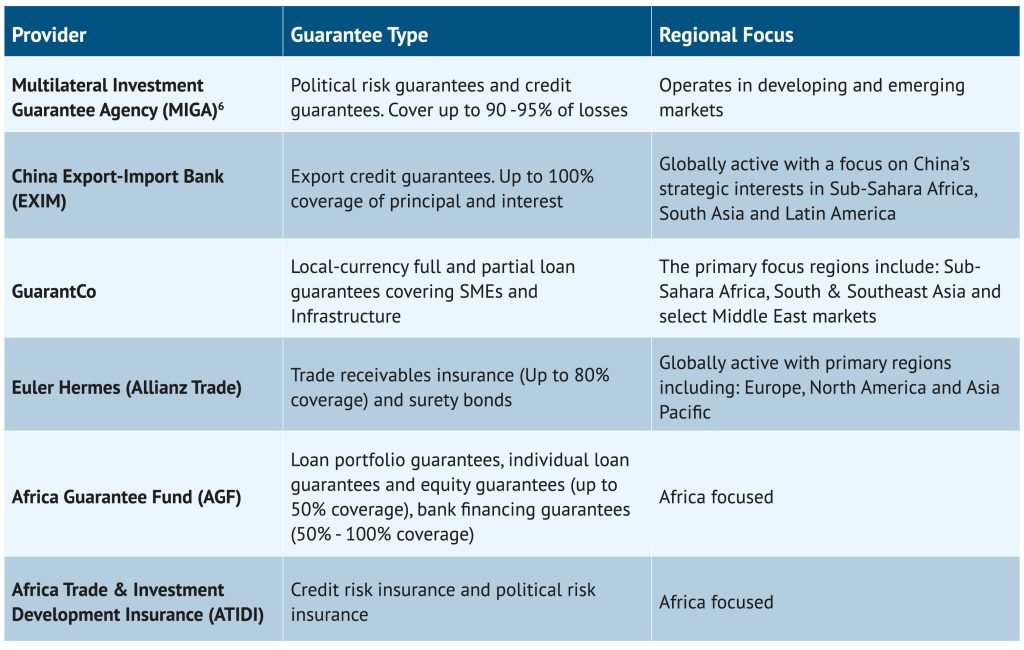

The global financial guarantee market was estimated at USD 42.3 billion at end-2024, with a 9.7% Compound Annual Growth Projection (CAGR) to USD 72.6 billion by 2033, driven by persistent finance gaps, trade finance needs and new priorities in green and climate projects. Suppliers include government schemes, sovereign guarantees, multilateral banks, and private firms. Products vary by provider (direct vs indirect), coverage (full vs partial, open-ended vs closed ended) and payout structure (indemnity, one time payout, step-in and loss-sharing). The major global guarantee firms include: the Multilateral Investment Guarantee Agency (MIGA), China Export-Import Bank (EXIM), GuarantCo, Euler Hermes (Allianz Trade) and Africa Guarantee Fund.

Table 1: Major Global Guarantee Firms

Source: World Bank, GuarantCo, China EXIM, Allianz Trade and AFC websites, Agusto & Co. Research

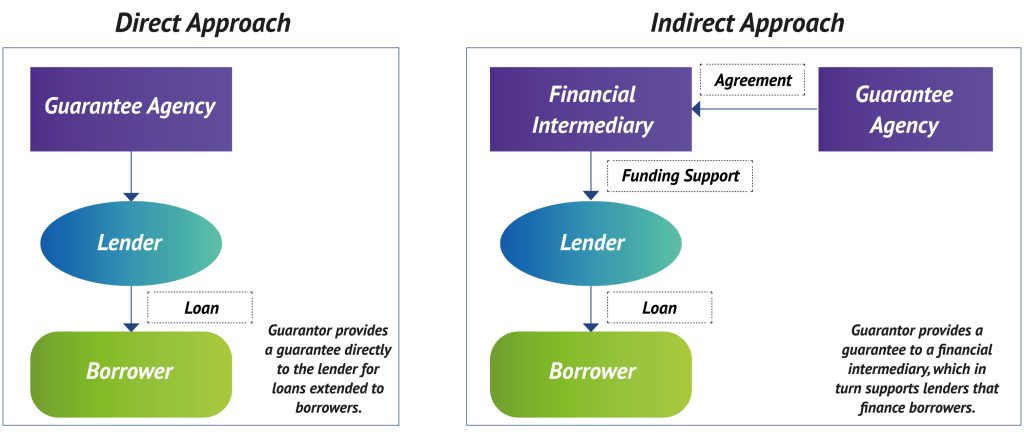

Figure 1: Credit Guarantee Mechanism- Direct vs Indirect Approach.

Source: Agusto & Co Research

Credit guarantees primarily de-risk lending, mobilise private capital, and extend credit access to high-risk segments where lender perceptions deter engagement. These instruments have proven effective in advanced markets: Japan’s Credit Guarantee Corporations cover 10-35% of SME loans; China’s EXIM/CDB schemes have facilitated USD 560 billion in commitments since 2000; France’s Bpifrance mobilised USD 44 billion in 2023 (including USD 24.4 billion export guarantees); and the UK’s British Business Bank delivered over USD 6.5 billion via ENABLE. Conversely, Kenya’s credit guarantee ecosystem remains nascent, constrained by limited institutional capacity and sectoral penetration. Yet it stands at an inflection point, evidenced by the Draft Central Bank of Kenya (Credit Guarantee Business) Regulations 2025, which signal regulatory maturation and growing recognition of guarantees’ potential to unlock affordable credit at scale.

Review of Existing Credit Guarantee Schemes

Credit guarantees have proven instrumental in enhancing finance access, driving financial inclusion, and mobilising long-term local capital for private sector development. GuarantCo Limited, a leading infrastructure specialist established in 2005, addresses funding gaps in low-income African and Asian markets by leveraging private capital for essential projects. Its guarantees bridge the divide between project requirements and local market terms, instilling confidence in banks and institutional investors. Offering full/partial credit guarantees, liquidity facilities, and portfolio frameworks, with payouts triggered on verified default, GuarantCo had facilitated USD 7.1 billion in investments by Q1 2026, 95% private sector-led. In Kenya, notable transactions include: a 50% partial guarantee on Acorn’s KSh 4.3 billion (USD 41.5 million) green note (2019), 75% coverage for Bboxx Kenya’s KSh 1.6 billion (USD 15 million) solar home systems serving 470,000 households (2021), and KSh 750 million (USD 9 million) for Kaluworks’ corporate bond (2012).

The African Guarantee Fund (AGF), established in 2011 by Denmark, Spain, and the African Development Bank (AfDB), is registered in Kenya under the Companies Act 2015. AGF facilitates SME access to finance across agriculture, manufacturing, and renewable energy, driving African economic growth. It offers loan portfolio guarantees (up to 50% coverage), individual loan guarantees (up to 50%), bank financing guarantees (50-100%), and equity guarantees (up to 50%). AGF guarantees activate upon borrower default causing actual lender loss. From inception to 31 December 2024, AGF issued USD 2.7 billion in guarantees, unlocking USD 5.5 billion in loans to 44,000 SMEs – a 2:1 leverage ratio demonstrating measured capital mobilisation.

Rwanda’s Partial Credit Guarantee (PCG) scheme, launched in 2012 and managed by the Business Development Fund (BDF), mitigates collateral gaps – a persistent barrier preventing MSMEs from securing bank financing. PCG covers 50% of loan amounts for general MSMEs, extending to 75% for women/youth-owned businesses and priority sectors. By sharing credit risk, PCG reduces banks’ perception of MSMEs as high-risk borrowers, enabling lending on favourable terms, boosting financial inclusion, and spurring economic growth. By 31 July 2025, BDF’s PCG had supported over 40,000 businesses, achieving 8x greater beneficiary reach than Kenya’s CGS despite comparable market contexts.

Credit guarantees have emerged as efficient catalysts for reshaping financial markets, enabling governments, development institutions, and lenders to channel investment finance by de-risking lending portfolios and unlocking private capital – thus bridging the persistent mismatch between high credit demand and lenders’ low risk appetite. By recalibrating credit perceptions, guarantees materially lower capital costs, rendering large-scale, long-term projects financially viable. Moreover, they strengthen financial systems through enhanced risk assessment practices, cultivated credit discipline, and accelerated adoption of innovative instruments.

Kenya’s Credit Guarantee Landscape

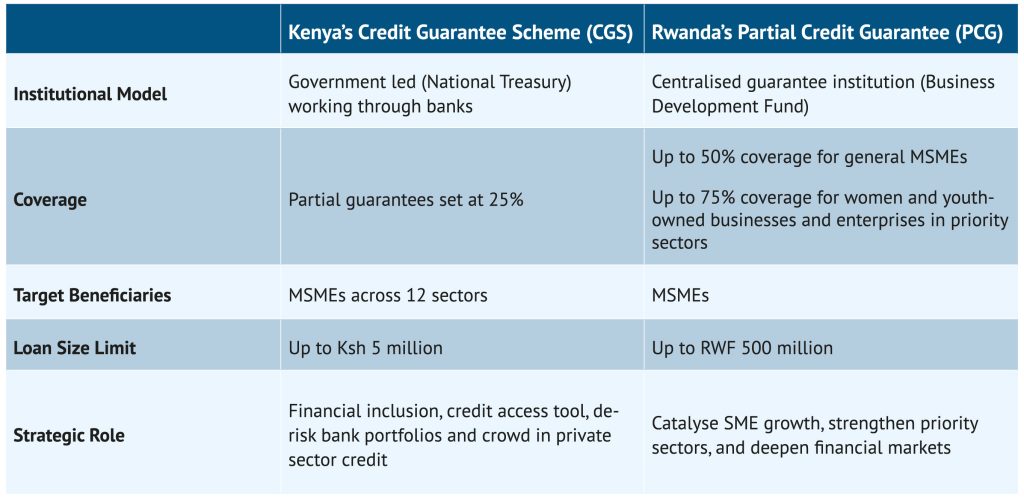

Over the past seven years, Kenya’s credit guarantee market has matured, blending government-backed schemes with specialised providers serving MSMEs and infrastructure developers. Launched in December 2020, the Credit Guarantee Scheme (CGS) establishes risk-sharing partnerships with Participating Financial Institutions (PFIs), offering 25% partial guarantees on loans to eligible MSMEs. This mechanism stimulates economic activity by catalysing additional lending and investment through public-private collaboration. With KSh 3 billion seed capital allocated in FY 2020/21 as a loss buffer, CGS had facilitated KSh 6.7 billion in credit to targeted MSMEs across 12 sectors and 46 counties by December 2025 – achieving 2.2x leverage from initial capital. The scheme enhances MSME performance by improving access to affordable credit, though its uniform 25% coverage yields lower per-business impact than Rwanda’s tiered 50-75% PCG.

Table 2: CGS Vs PCG

Source: Kenya National Treasury, World Bank

The Rural Kenya Financial Inclusion Facility (RK-FINFA) operates the Rural Credit Guarantee Scheme (R-CGS) under the National Treasury’s CGS framework. Launched in 2023, R-CGS provides risk-sharing mechanisms to catalyse mainstream financial institutions’ rural agriculture outreach, targeting 68,000 smallholder households (50% women, 30% youth). It employs three modalities: direct lending to farmers/agribusiness MSMEs using PFIs’ credit systems; value chain financing for aggregators/processors; and wholesale funding via SACCOs/Microfinance Banks for small-scale rural investments. This addresses liquidity constraints while establishing sustainable agricultural growth foundations.

Dhamana Credit Guarantee Company enables local currency credit access through loans/bonds for public/private infrastructure players. Focusing on energy, social infrastructure, agri-infrastructure, transport, and water/sanitation, Dhamana completed its debut transaction in Q4 2025: a KSh 2.5 billion facility supporting Safaricom’s telecom tower solarisation—demonstrating infrastructure guarantees’ catalytic potential ahead of broader CGS/MSME focus.

The Regulatory Landscape

Kenya’s credit guarantee landscape has evolved through Treasury-led CGS and commercial banks’ internal SME/agribusiness products, operating via contractual arrangements due to absent unified prudential oversight. The landmark Business Laws (Amendment) Act 2024 establishes Central Bank of Kenya (CBK) supervision of guarantee providers – shifting from fragmented risk management to institutionalised standards, risk-based pricing, and claim verification mechanisms. This regulatory maturation addresses moral hazard gaps while enabling private entry, mirroring Rwanda BDF/PCG’s centralised model that achieved 8x Kenya CGS beneficiary scale.

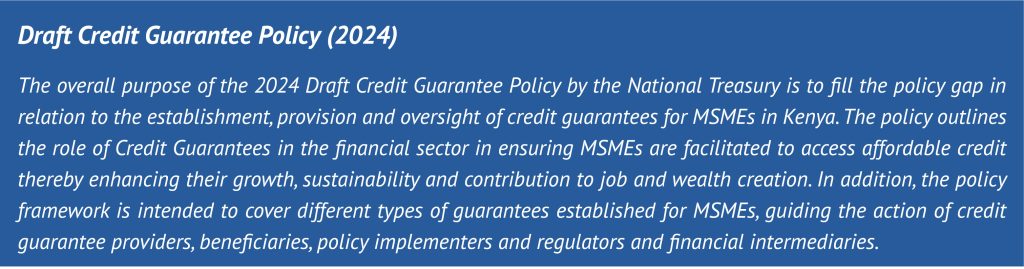

Draft Credit Guarantee Policy (2024)

Opportunities in the Kenyan Market

Credit guarantees present strategic, commercial, and developmental opportunities by addressing MSME credit barriers—98% of Kenyan businesses contributing over 30% to GDP yet facing collateral shortages and risk aversion from commercial and microfinance banks. These instruments reshape lending structures, catalyse sectoral growth, mobilise institutional capital, and enhance financial stability. By sharing lending risk, guarantees unlock credit access for underserved MSMEs, incentivising banks to extend financing where previously deterred. This drives financial inclusion, MSME formalisation, and sustainable scaling, evidenced by Rwanda PCG reaching 40,000 beneficiaries versus Kenya CGS’s 5,000. Simultaneously, guarantees mitigate lenders’ default exposure, enabling portfolio diversification into higher-risk (priority) sectors, higher lending volumes, and improved credit flows to underserved markets.

Beyond access, credit guarantees lower borrowing costs by recalibrating lenders’ risk perceptions, enabling modest interest rate reductions, extended tenors, and flexible repayment structures. Enhanced instrument creditworthiness attracts pension funds (KSh 2.5 trillion assets) and institutional investors, deepening domestic capital markets, reducing external financing dependence, and improving liquidity. Corporate/government bond access at compressed yields facilitates capital-intensive infrastructure, driving bond issuance and targeted sectoral expansion.

Despite the market enabling benefits, credit guarantees carry inherent risks that can undermine effectiveness. Key concerns include moral hazard which often result in high default rates and deteriorating portfolio quality, adverse selection leading to inefficient allocation of credit and market distortion caused by crowding out of private risk-sharing mechanism. These risks can however be mitigated through strong structural designs features, effective approaches such as graduated risk-sharing structures and risk-based pricing to promote financial sustainability.

Conclusion

Kenya’s credit guarantee market stands at an inflection point, with maturing CBK regulation establishing transformation foundations. Strategic collaborations among financial institutions, private sector, development partners, and guarantee providers will develop/de-risk bankable projects via targeted mechanisms, ensuring ecosystem sustainability. Formalised rating agency partnerships will refine risk profiling, enhance pricing accuracy, and build investor confidence – channelling pension funds (KSh 2.5 trillion assets) into guaranteed instruments. As regulatory clarity strengthens and private sector enters the market, credit guarantees will proliferate near-to-medium term, unlocking capital flows and systematically reducing systemic risk.